Strategy’s Q1 2026 earnings deck had one slide that quietly changed the way investors should understand the company.

For years, the Strategy playbook looked simple:

Raise capital → buy Bitcoin → increase Bitcoin per share.

That was the core engine. Sell MSTR. Buy BTC. Repeat when market conditions were favorable.

But in Q1 2026, management showed that the machine has evolved. Strategy is no longer operating with just one engine. It is building a multi-engine capital allocation system where it can sell common equity, sell preferred equity, build USD reserves, retire debt, issue digital credit, and even sell Bitcoin if doing so improves Bitcoin per share or strengthens the capital structure.

That is the real message behind the “Adding More Engines” slide. Strategy is no longer just a Bitcoin holding company. It is becoming a Bitcoin-backed capital markets platform.

The Core KPI: Bitcoin Per Share

Before understanding the optionality, we need to understand the scoreboard.

Strategy is no longer asking investors to judge the business primarily through traditional EPS. Because of fair-value accounting, quarterly earnings will swing massively with Bitcoin’s quarter-end price. In Q1 2026, Strategy reported a large operating loss and net loss mainly because Bitcoin fell during the quarter, not because the underlying capital strategy stopped working. The deck explains that Strategy adopted fair-value accounting in 2025, so the carrying value of Bitcoin now equals quarter-end market value, creating income statement volatility.

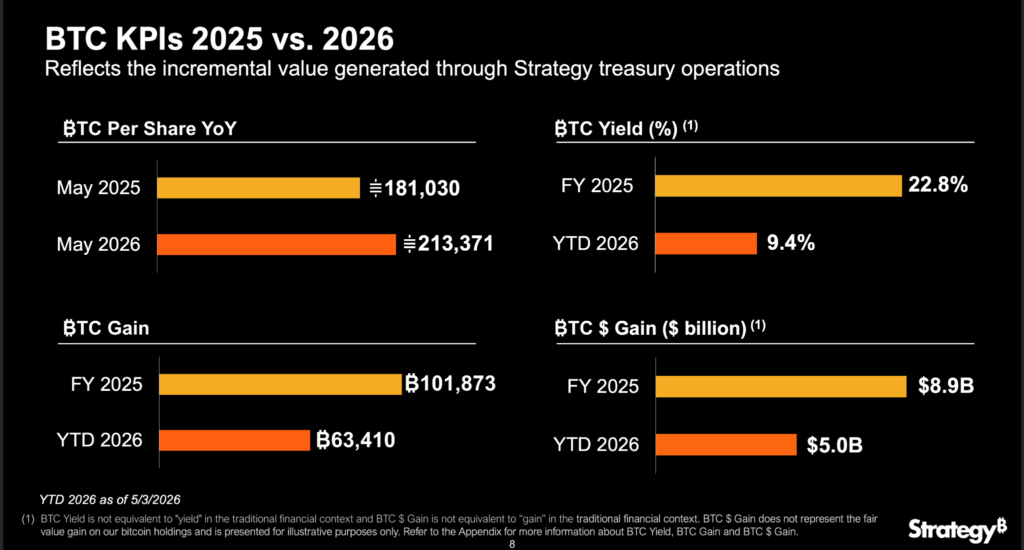

The real KPI is Bitcoin per share.

Strategy’s BTC per share rose from 181,030 sats per share in May 2025 to 213,371 sats per share by May 2026. The company also reported 9.4% BTC Yield YTD 2026, compared with 22.8% for full-year 2025, and 63,410 BTC Gain YTD 2026, compared with 101,873 BTC Gain for full-year 2025.

This is the foundation of the entire model.

Strategy is not simply trying to own more Bitcoin. It is trying to increase the amount of Bitcoin backing each MSTR share.

That is why optionality matters.

The Old Strategy Was Powerful, But Simple

The original Strategy trade was:

Sell MSTR → Buy BTC

When MSTR traded at a premium to its Bitcoin holdings, Strategy could issue common stock, buy Bitcoin, and increase Bitcoin per share.

That model worked because MSTR functioned like amplified Bitcoin. If the company issued shares at a premium to net asset value and used the proceeds to buy Bitcoin, existing shareholders could benefit from Bitcoin per share accretion.

But this model depended heavily on one condition MSTR must trade at a high enough mNAV.

If MSTR trades at a strong premium, common equity issuance can be accretive. If MSTR trades too close to its Bitcoin NAV, the trade becomes less attractive. And if MSTR trades below the breakeven level, issuing common equity can become harmful.

That is why the Q1 deck is so important. Strategy is telling investors that it now has more than one way to create Bitcoin per share accretion.

Strategy’s Multi-Engine Model

The “Adding More Engines” slide shows Strategy’s capital allocation model split into current trades and future trades.

The current trades are:

Sell MSTR → Buy BTC

Sell MSTR → Buy USD

Sell STRC → Buy BTC

The future trades are:

Sell MSTR → Buy Debt

Sell STRC → Buy USD

Sell STRC → Buy Debt

Sell BTC → Buy USD

Sell BTC → Buy Debt

This slide is the heart of the new Strategy model.

Earlier, the company had one dominant engine: common equity issuance. Now it has multiple engines: MSTR, STRC, USD reserves, Bitcoin reserves, other preferred instruments, and potentially BTC derivatives. The deck explicitly frames these as sources and uses of capital, with sources including MSTR, STRC, USD reserve, BTC, other preferreds, and potential BTC derivatives; uses include BTC, USD dividends, USD reserve, debt, and preferred securities.

In simple language, Strategy is no longer only asking:

“How do we buy more Bitcoin?”

It is asking:

“Which trade increases Bitcoin per share the most while keeping the balance sheet safe?”

That is a much more advanced game.

STRC Changed the Optionality of the Entire Company

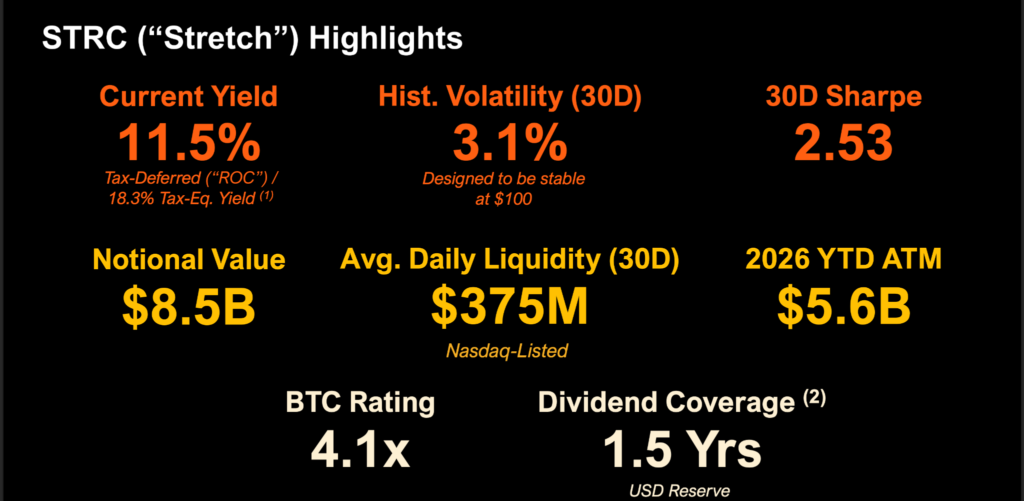

The reason Strategy can talk about this expanded playbook is because STRC has become a real funding engine.

STRC is $8.5 billion instrument with 11.5% current yield, around $375 million of 30-day average daily liquidity, 3.1% historical volatility, and a 2.53 30-day Sharpe ratio. Strategy also describes STRC as designed to be stable around $100 par.

STRC is important because it gives Strategy a way to raise capital without issuing common stock. Selling MSTR can dilute common shareholders. Selling STRC creates a preferred obligation, but it does not dilute common shareholders in the same direct way.

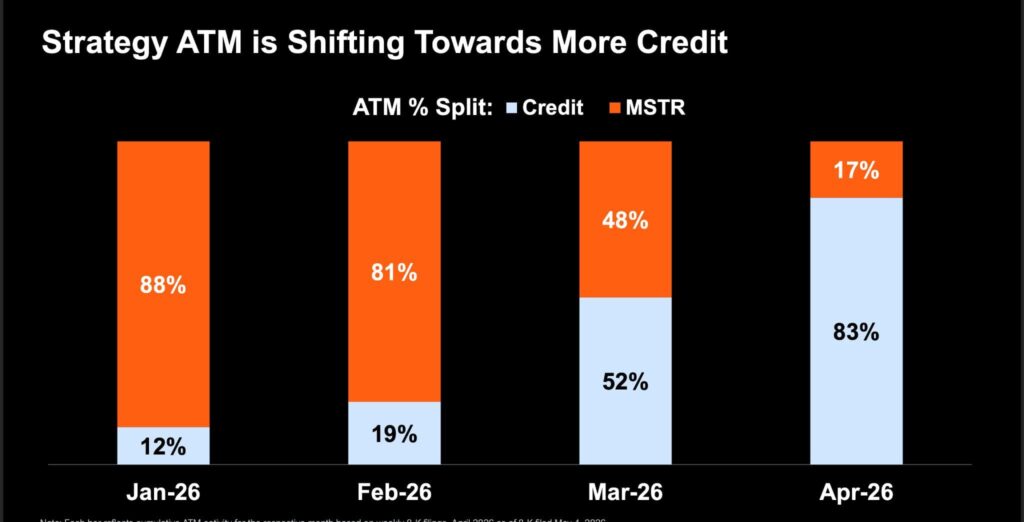

Phong Le made this point clearly in the earnings call: Strategy’s ATM activity has shifted heavily toward digital credit. In January, most issuance was MSTR common equity; by April, most issuance was digital credit, which management described as less dilutive to common shareholders.

That shift matters because STRC gives Strategy a second major engine.

The old engine was:

Common equity premium → Bitcoin purchases

The new engine is:

Digital credit demand → Bitcoin purchases / USD reserve / debt retirement

This is what increases Strategy’s optionality.

The STRC Cost of Capital Is Not Fixed at 11.5%

One of the most misunderstood parts of STRC is the cost of capital.

Many investors look at STRC and say:

“Strategy is borrowing at 11.5%.”

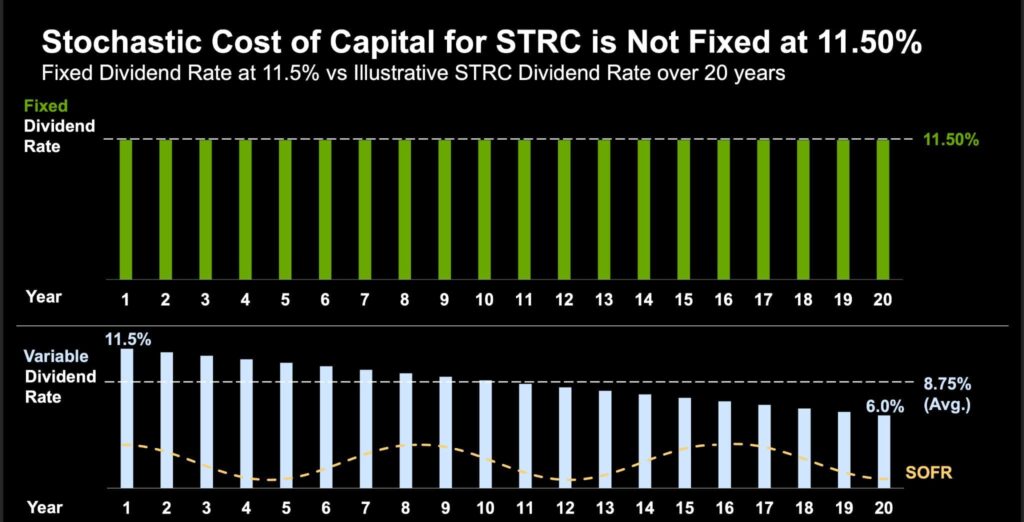

But management pushed back against that framing in the transcript. Saylor explained that STRC is not a traditional loan because it is perpetual capital. When Strategy sells STRC, it does not have a fixed maturity where the principal must be repaid. He also explained that the cost of capital is not permanently fixed at 11.5%; it is stochastic and depends on SOFR, credit spreads, market demand, and Strategy’s ability to adjust the dividend rate over time.

This image directly addresses this. It contrasts a fixed 11.5% dividend assumption with an illustrative STRC dividend path over 20 years showing an 8.75% average dividend rate.

This is extremely important.

If investors assume STRC always costs 11.5%, the model looks more expensive. But if STRC volatility falls, liquidity improves, demand deepens, and credit spreads compress, Strategy may be able to lower the dividend rate over time.

The company’s rate guidance also shows how this mechanism is intended to work. If STRC trades below the target range, management may recommend raising the rate; if it trades above $101 VWAP, management may recommend lowering the rate and/or doing a follow-on offering.

This turns STRC into a dynamic capital instrument.

If STRC trades weak, Strategy can raise the yield to pull it back toward par.

If STRC trades strong, Strategy can lower the yield or issue more STRC.

If interest rates fall, the floor and credit spread structure may give Strategy more room to reduce the cost of capital.

If credit spreads compress over time, the cost of digital credit can decline.

This is why STRC is not simply “expensive debt.” It is a programmable preferred instrument with embedded issuer optionality.

Equity Model: The Trade Is Not Always the Same

Strategy is no longer showing one capital allocation path. It is showing multiple scenarios depending on mNAV, BTC price appreciation, STRC issuance, dividend costs, USD reserve needs, and risk metrics.

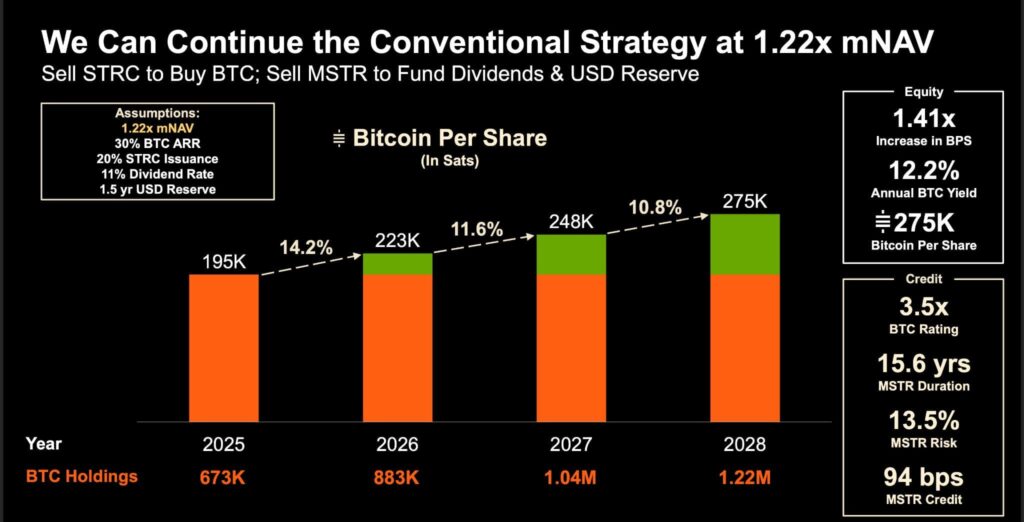

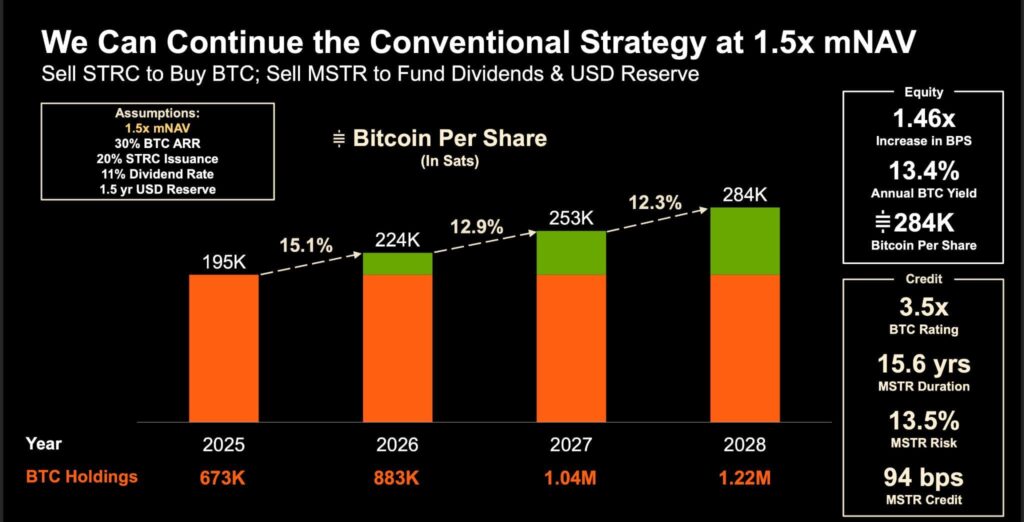

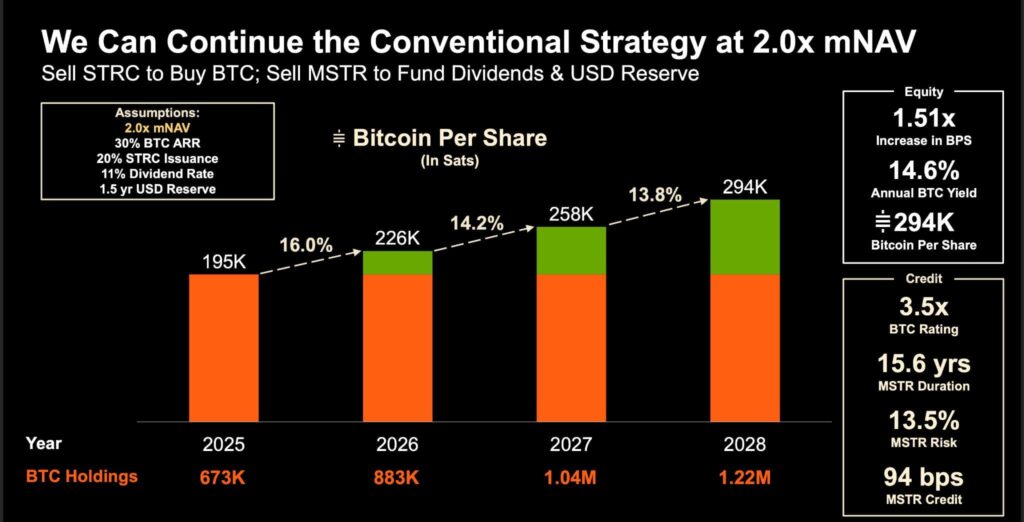

The deck shows conventional strategy scenarios where Strategy sells STRC to buy BTC and sells MSTR to fund dividends and USD reserves.

At 1.22x mNAV, the model produces 275K Bitcoin per share

At 1.5x mNAV, the model produces 284K Bitcoin per share and 13.4% annual BTC Yield.

At 2.0x mNAV, it produces 294K Bitcoin per share and 14.6% annual BTC Yield.

The message is simple:

Higher mNAV gives Strategy more accretion power.

At higher mNAV, selling MSTR becomes more efficient. The company can raise more dollars per unit of dilution, buy more BTC, and generate higher BTC per share growth.

But the key point is that even at lower mNAV levels, Strategy still has tools.

The transcript says that even in weaker market conditions, the company believes it can continue to deliver BTC Yield by using combinations of STRC issuance, MSTR issuance, USD reserve management, and BTC sales. Saylor described these as different scenarios showing how market sentiment drives the business: negative sentiment still allows a “pretty good business,” while positive sentiment allows Strategy to double Bitcoin per share faster.

This is the core optionality.

Strategy does not need perfect market conditions to operate. Strong market conditions accelerate the model, but weaker conditions do not necessarily break it.

Risk Model: Every Trade Has an Equity Impact and a Credit Impact

Strategy’s model is not just about BTC Yield. It also tracks risk.

The transcript explains that management uses an equity and risk model to calculate the benefits to equity and the deltas to risk for every capital markets transaction. The model considers metrics such as BTC Rating, liability duration, MSTR Risk, and fair credit spread.

This is very important because every trade has two sides:

Equity side: Does this increase BTC per share?

Credit side: Does this increase or reduce balance sheet risk?

For example, building a USD reserve may be negative for BTC per share because dollars are not Bitcoin. But it is positive for credit quality because it supports dividend coverage and reduces perceived risk.

Similarly, selling BTC to fund dividends may slightly increase risk because the BTC reserve declines, but it can avoid common stock dilution. In some conditions, that may be better for MSTR holders.

This is why Strategy’s capital allocation cannot be understood with one simple rule. The company is constantly balancing BTC Yield against BTC Rating, credit spread, duration, and risk.

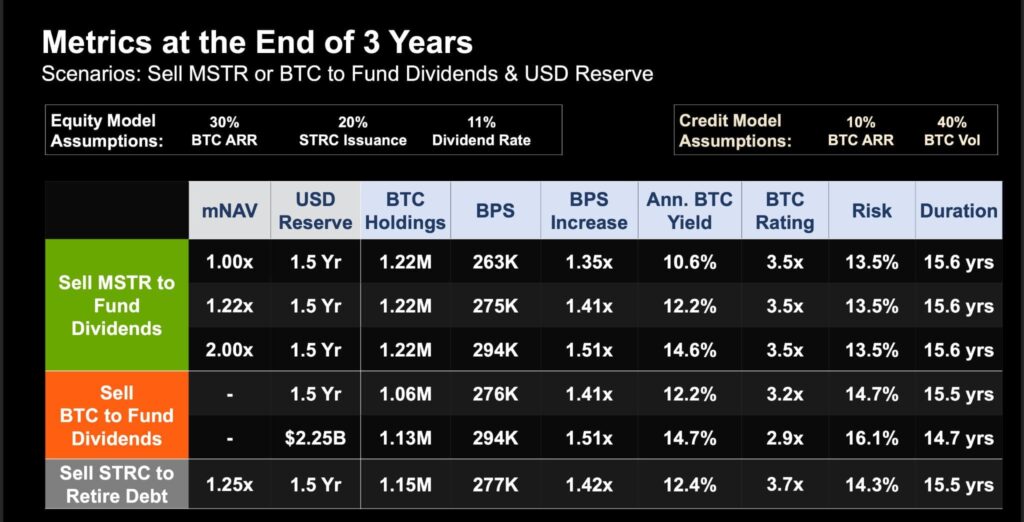

Scenario 1: Sell MSTR to Fund Dividends and USD Reserve

The conventional model assumes Strategy continues selling STRC to buy BTC and sells MSTR to fund dividends and maintain a USD reserve.

At 1.22x mNAV, the deck shows this can generate 12.2% annual BTC Yield, 275K Bitcoin per share, 3.5x BTC Rating, 13.5% MSTR Risk, and 15.6 years of MSTR Duration.

This is the base case of the new machine.

STRC funds Bitcoin purchases.

MSTR funds cash obligations.

The USD reserve stays stable.

Bitcoin per share continues rising.

In this model, common equity is still used, but it is not the only engine.

Scenario 2: Sell BTC to Fund Dividends

This is the controversial scenario.

Strategy shows that it can fund dividends by selling Bitcoin and still increase Bitcoin per share under certain assumptions. In the transcript, Saylor explains that Strategy can fund dividends by selling Bitcoin while still growing total BTC holdings over time. One scenario showed the company moving from roughly the 670K BTC level toward 850K, 950K, and eventually 1 million BTC, while funding obligations with Bitcoin.

This is where many investors need to rethink the model.

Selling Bitcoin is not automatically bearish if the company is simultaneously issuing STRC, buying more BTC than it sells, avoiding common dilution, and increasing BTC per share.

Saylor compared this to a real estate development company that sells land at a profit to fund obligations and then buys more land. The business does not fail because it sells some inventory; it works if the company sells intelligently and continues growing the asset base.

This is why the “never sell Bitcoin” narrative is too simplistic.

The more precise Strategy doctrine is:

Be a net accumulator of Bitcoin and increase Bitcoin per share over time.

That leaves room to sell Bitcoin tactically if the trade improves the structure.

Scenario 3: Sell STRC to Retire Debt

Another powerful scenario is:

Sell STRC → Buy Debt

The deck’s scenario table shows a “Sell STRC to Retire Debt” case with 277K Bitcoin per share, 1.42x BPS increase, 12.4% annual BTC Yield, 3.7x BTC Rating, 14.3% MSTR Risk, and 15.5 years of MSTR Duration. The assumption is that 20% of annual STRC proceeds are used to retire debt.

This matters because Strategy still has convertible debt outstanding. Retiring converts can reduce future dilution risk and improve the capital structure.

Saylor explained that if Strategy diverted 20% of Stretch issuance to retire debt, it could retire all debt over the next three years, bringing debt from $8.2 billion to zero, reducing net leverage to zero, and increasing the duration of the company’s instruments to around 15 years.

This is an underrated bullish lever for MSTR holders.

STRC is not just a way to buy Bitcoin. It can also be used to remove future dilution and reduce balance sheet risk.

Scenario 4: Sell BTC or STRC to Buy Back MSTR

One of the most interesting parts of the transcript is the possibility of buying back common stock.

Saylor explained that if MSTR traded below the breakeven mNAV, swapping BTC for MSTR could become extremely accretive. He gave an example where if the market irrationally pushed MSTR to a very low mNAV, buying back common stock with BTC could create large BTC Yield and BTC Gain.

He also discussed the possibility of selling STRC to buy back MSTR. In his framing, this would allow Strategy to create amplification by selling credit and buying common equity. He even described this as Strategy potentially doing a kind of “LBO on its own common stock” if the market misprices MSTR.

This is a huge optionality point.

If MSTR trades at a premium, Strategy can sell MSTR to buy BTC.

If MSTR trades at a discount, Strategy can potentially sell BTC, USD, or STRC to buy MSTR.

That means Strategy can potentially benefit from both overvaluation and undervaluation, depending on which trade is accretive.

This is what makes the model much more dynamic than a passive BTC treasury.

The 1.22x mNAV Breakeven Is Critical

A major concept in the call is that Strategy’s breakeven mNAV is not 1.0x anymore.

Because the capital structure now includes debt and preferred equity, the breakeven level for issuing MSTR to buy Bitcoin is higher. The deck and transcript reference 1.22x mNAV as an important threshold. At or above this level, the conventional strategy of selling MSTR to support the model becomes more attractive. Below it, other trades may become more attractive.

This means investors should stop thinking in binary terms:

“MSTR trades above NAV, so issuance is good.”

“MSTR trades below NAV, so issuance is bad.”

The better question is:

“Relative to the current capital structure, which trade is most BTC-per-share accretive?”

At high mNAV, sell MSTR.

At strong STRC demand, sell STRC.

At low mNAV, consider buybacks.

At weak credit conditions, build USD reserve.

At debt mispricing, retire converts.

At favorable BTC tax lots, sell high-cost-basis Bitcoin to fund obligations.

That is the real playbook.

The Balance Sheet Gives Strategy Room to Use These Options

Optionality only matters if the balance sheet can survive volatility.

Strategy’s Q1 deck shows a $64 billion BTC reserve, $13.5 billion of preferred equity, $8.2 billion of convertible debt, 1.27x mNAV, 9% net leverage, and 34% amplification.

Suggested image placement:

[Insert Slide 15: Strategy’s Balance Sheet is a Digital Fortress]

The deck also says the company’s convertible debt is covered even after a hypothetical 91% BTC price decline, with the BTC price falling to roughly $7.3K and BTC reserve still covering net debt at 1.0x BTC Rating.

Suggested image placement:

[Insert Slide 18: Converts Are Fully Covered Even After 91% BTC Price Decline]

This balance sheet strength is what allows management to be opportunistic.

A weak balance sheet has no optionality. It is forced to sell what it can, when it can.

A strong balance sheet can choose between funding sources, wait for better windows, retire liabilities, build reserves, or buy back mispriced equity.

Strategy is trying to move from forced financing to strategic financing.

Why STRC Demand Can Become a Flywheel

STRC’s success creates a flywheel for the whole company.

The deck shows that Strategy’s goal is to double Bitcoin per share in seven years through digital credit. It highlights three levers that enhance this objective: lower cost of credit, higher digital credit sales, and higher mNAV.

The flywheel looks like this:

STRC becomes more liquid → volatility falls → Sharpe ratio improves → demand rises → Strategy issues more STRC → buys BTC or retires debt → BTC per share rises → MSTR becomes stronger → mNAV improves → Strategy gains more accretive capital options.

That is why the cost of capital is so important.

If STRC stays at 11.5%, the machine still works under the company’s assumptions. But if STRC’s long-term average cost of capital falls toward the illustrative 8.75% level shown in the deck, the model becomes much more powerful.

Lower STRC cost means more spread between Bitcoin’s long-term appreciation and Strategy’s funding cost.

That spread is the engine.

Why This Is Bullish for MSTR Holders

For MSTR holders, the optionality is bullish because Strategy now has multiple ways to protect and grow Bitcoin per share.

In strong markets, Strategy can sell MSTR at high mNAV and buy BTC.

In credit-friendly markets, Strategy can sell STRC and buy BTC.

If debt is inefficient, Strategy can sell STRC and retire converts.

If the stock is undervalued, Strategy can potentially sell BTC, USD, or STRC to buy back MSTR.

If credit investors need more comfort, Strategy can build USD reserves.

If STRC trades above par, Strategy can lower the rate or issue more STRC.

If STRC trades below par, Strategy can raise the rate to support demand.

That is a very different company from the old version of MicroStrategy.

The old version had one main trade.

The new Strategy has a capital allocation matrix.

Why This Also Matters for STRC Holders

For STRC holders, optionality matters differently.

They care less about upside BTC per share growth and more about stability, liquidity, dividend coverage, and credit quality.

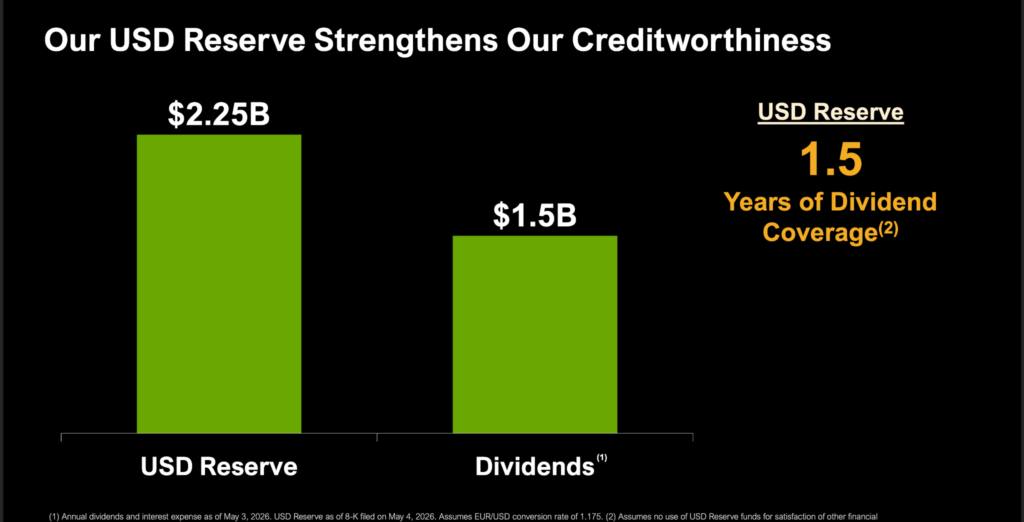

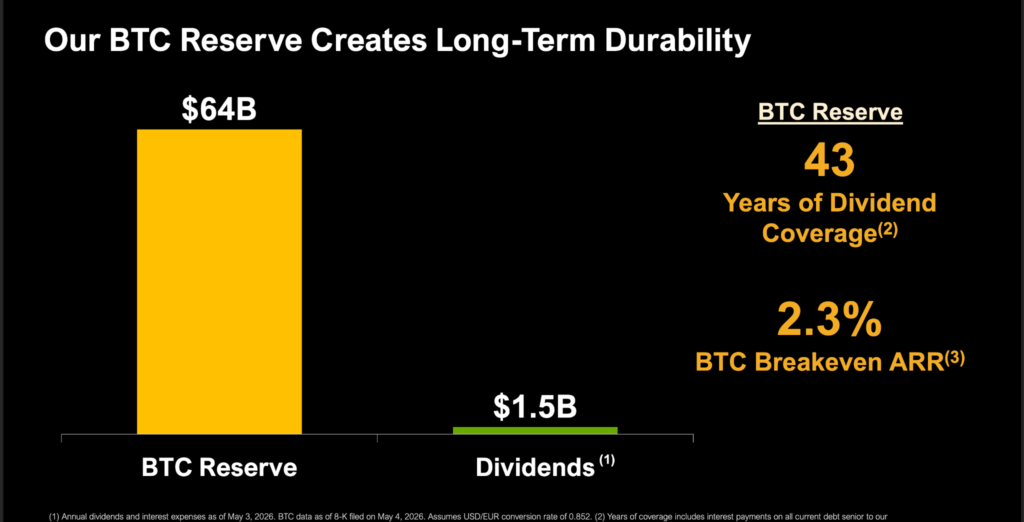

The deck shows Strategy has a $2.25 billion USD reserve, equal to about 1.5 years of dividend coverage, and a $64 billion BTC reserve, which the company says represents around 43 years of dividend coverage under its assumptions. It also shows a 2.3% BTC breakeven ARR, meaning Bitcoin would need to grow by only 2.3% annually for the BTC reserve growth to cover current obligations.

For STRC holders, the most important thing is that Strategy has multiple ways to fund dividends:

It can use USD reserves.

It can issue MSTR.

It can issue STRC.

It can sell BTC.

It can manage the rate.

It can retire debt.

It can improve credit quality.

That makes STRC more than a simple preferred stock. It becomes a Bitcoin-backed digital credit product supported by a large BTC reserve and a flexible capital markets engine.

The Risk: Optionality Requires Discipline

The bullish case depends on management using the tools intelligently.

More options do not automatically create value. They create value only when used at the right price.

Selling MSTR at low mNAV can be harmful.

Selling BTC at the wrong time can reduce upside.

Issuing too much STRC can increase dividend obligations.

Holding too much USD can drag Bitcoin per share growth.

Retiring debt at the wrong price can waste capital.

Reducing STRC’s dividend too quickly can hurt demand.

This is why the equity and risk model matters.

Strategy is not saying it will use every trade all the time. It is saying it can evaluate each trade based on BTC Yield, BTC Gain, BTC Rating, MSTR Risk, MSTR Duration, and fair credit spread.

That is the key difference between optionality and recklessness.

Conclusion: Strategy Is Becoming a Bitcoin Capital Allocator

The most important takeaway from Q1 2026 is not the accounting loss.

It is not even the fact that Strategy now holds over 818,000 BTC.

The real takeaway is that Strategy has expanded its capital allocation playbook.

The company now has multiple engines:

MSTR common equity

STRC digital credit

Other preferred instruments

USD reserve

BTC reserve

Convertible debt retirement

Potential BTC derivatives

Future common stock buybacks

Dynamic STRC rate adjustments

The old model was:

Sell stock → buy Bitcoin

The new model is:

Use the entire capital structure to increase Bitcoin per share while managing credit risk.

That is why Strategy is becoming harder to analyze using traditional equity frameworks. It is part Bitcoin treasury, part digital credit issuer, part capital markets machine, and part active balance sheet allocator.

For MSTR holders, the question is no longer only:

“How much Bitcoin does Strategy own?”

The better question is:

“How many ways can Strategy increase Bitcoin per share?”

After Q1 2026, the answer is clear: many more than before.